In my last post on Thursday 30th July I was looking at the downside targets on all the topping patterns on the main US indices and since then we have seen a very strong reversal back up, with those downside patterns failing into new all time highs on SPX and DIA, and failing today on IWM. This is now another big inflection point where US equity indices could turn down hard or continue higher, and I’ll be looking at that today.

Part of the reason for this has been the Iran War news where yet another imminent deal was announced on Sunday, though yesterday Iran denied any imminent deal or current ceasefire and underlined that by attacking the US base in Kuwait last night.

This morning Trump is back to issuing bloodcurdling threats to force Iran back to the negotiating table, and talking about a deal that might be concluded tomorrow, but unless he is now threatening a nuclear strike it’s hard to see that being any more successful than the previous ten or eleven times this has happened since March. Even in that case Iran would clearly appeal to their allies China and Russia and I suspect China at least would intervene to deter any use of nuclear weapons in this war.

I wrote in early May that both the US and Iran had been waiting for the other to concede defeat since March. That remains the case and it seems a long shot to think that Iran will now concede their control of the Strait of Hormuz as that has been a very clear red line for them since the start of the war. We’ll see what happens next but at the moment this looks like a Mexican standoff with the US threatening to devastate Iran, while Iran promises to respond by devastating oil and gas infrastructure in the rest of the Persian Gulf. The short term options for the US appear to be to resume the hot war on a similar limited basis to previous unsuccessful bombing campaigns, or to concede that Iran controls the Strait of Hormuz and try to spin that as a win.

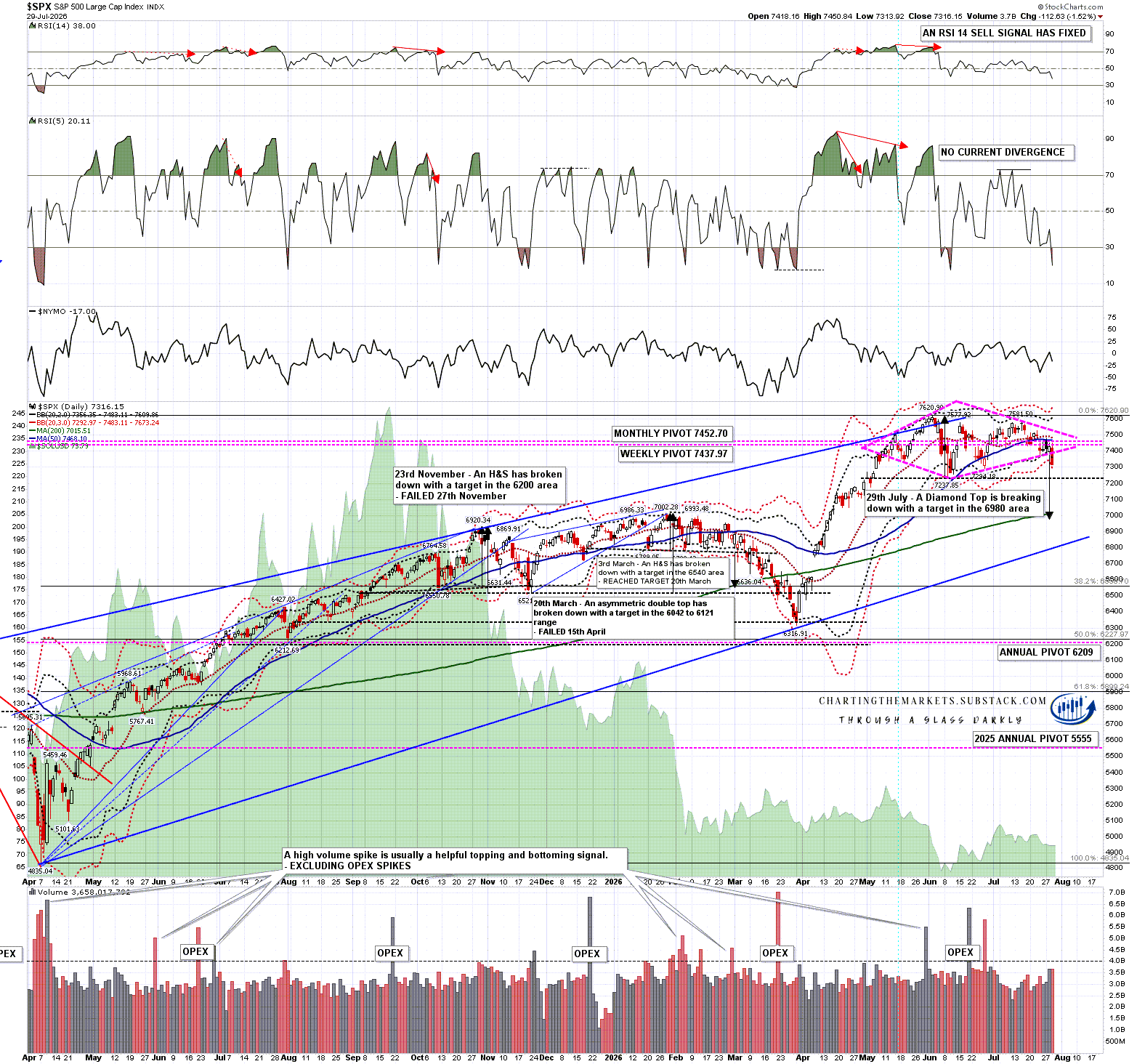

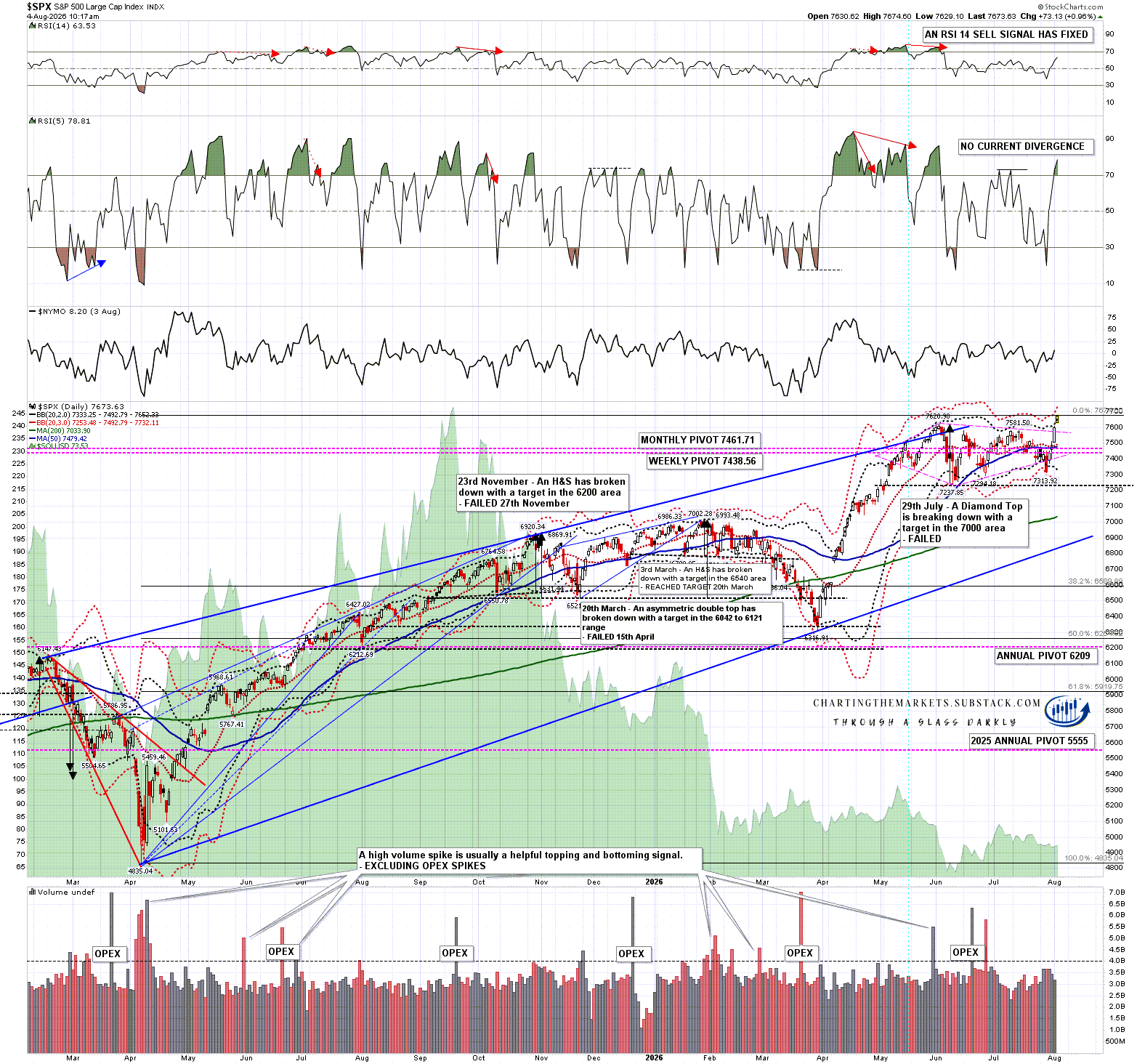

Looking at the US equity markets SPX made a new high today and could go higher. I’ll be doing another post in a day or two looking at that. Short term though SPX is close to the daily 3sd upper band and at minimum I’d be looking for a consolidation in this area for a week or so to allow the daily middle band to turn up more, and for the daily bands to expand to allow more room under the daily 3sd upper band.

On the bear side there is now a high quality double top setup on SPX.

SPX daily chart:

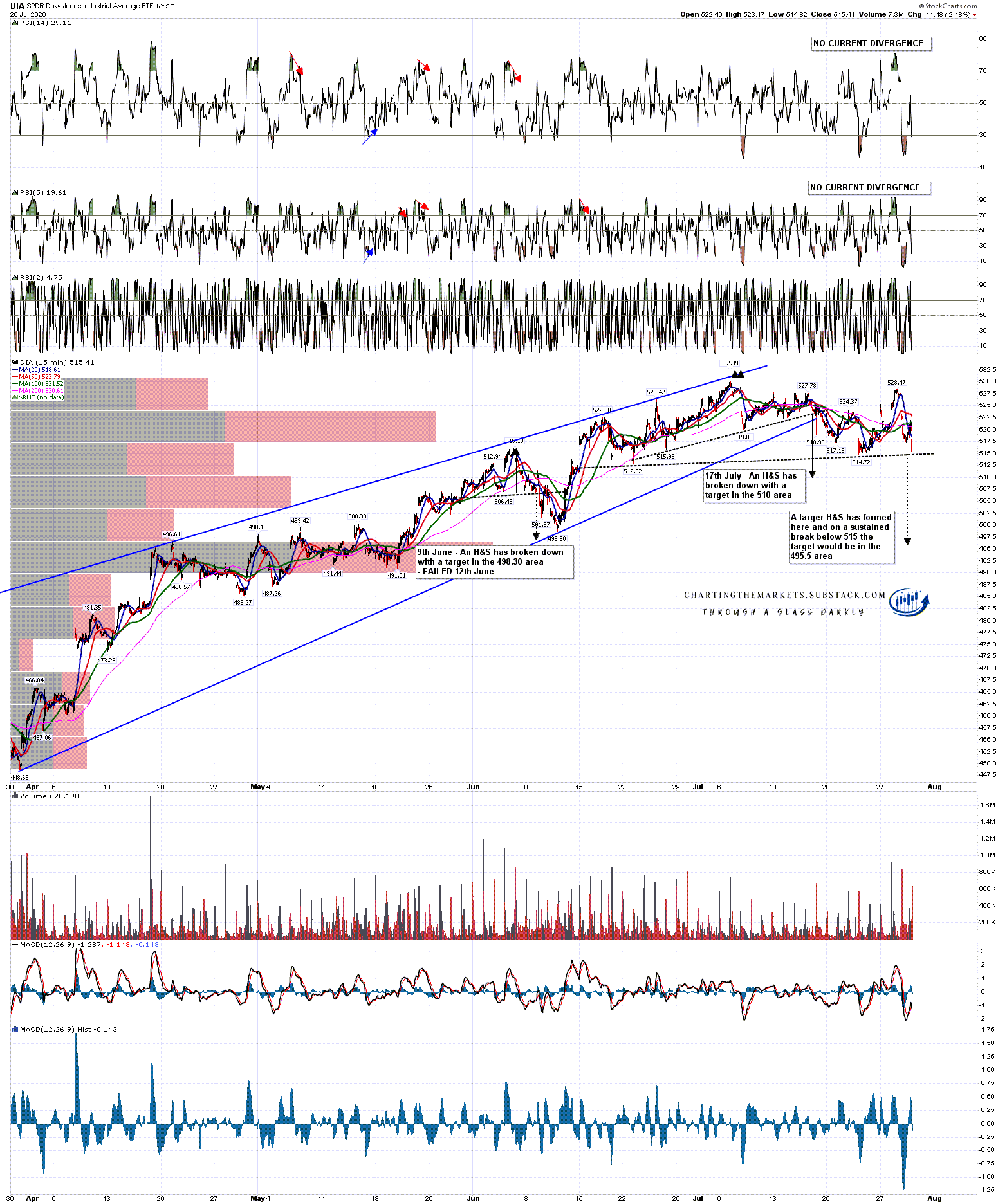

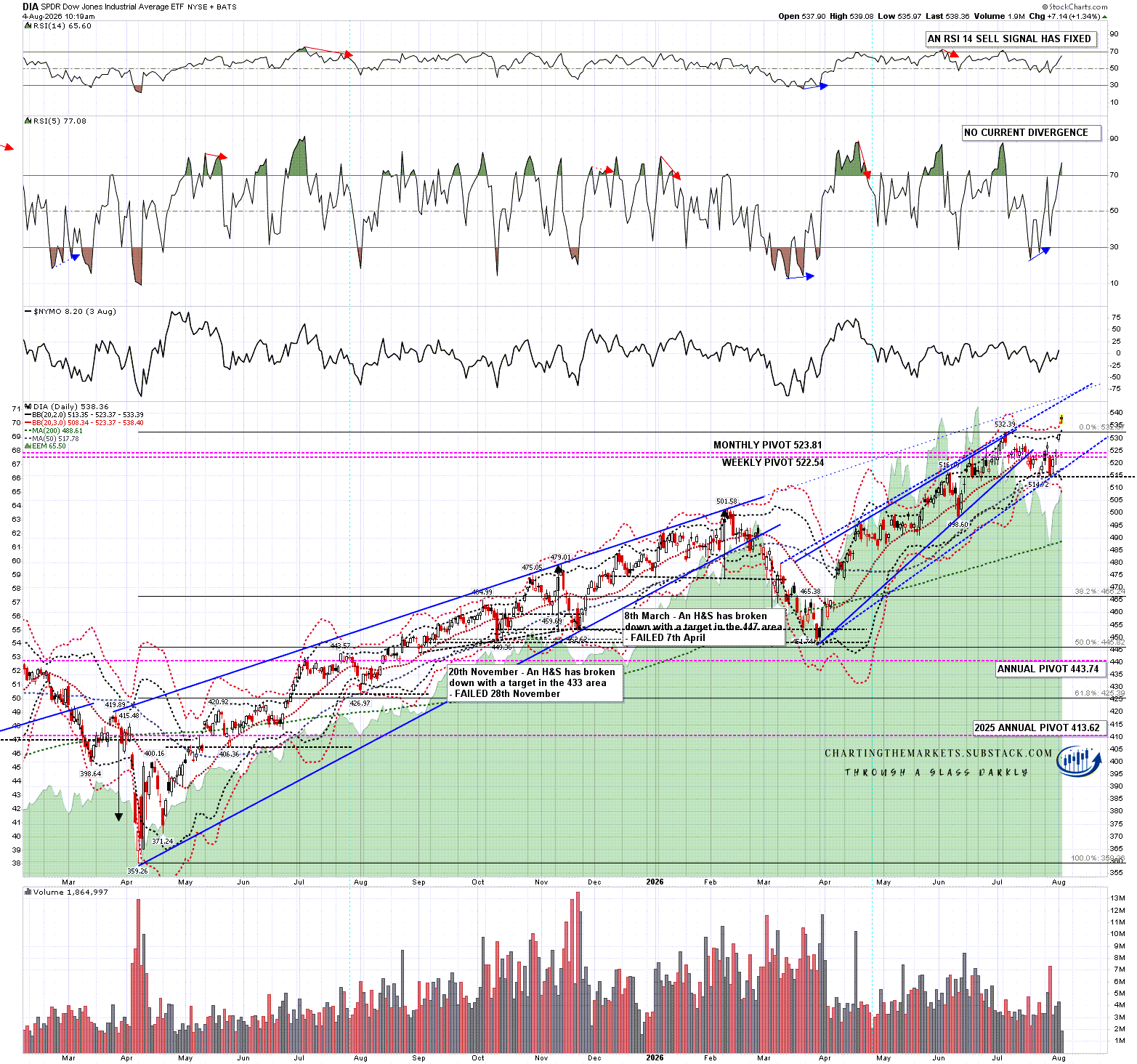

The H&S on DIA failed yesterday and DIA made a new all time high today. DIA was hitting the daily 3sd upper band as I capped the chart below and this also likely needs another week or so to consolidate if DIA is heading higher. Again I have a possible upside target and that is getting close in the 547 area.

On the bear side there is now a high quality double top setup on DIA.

DIA daily chart:

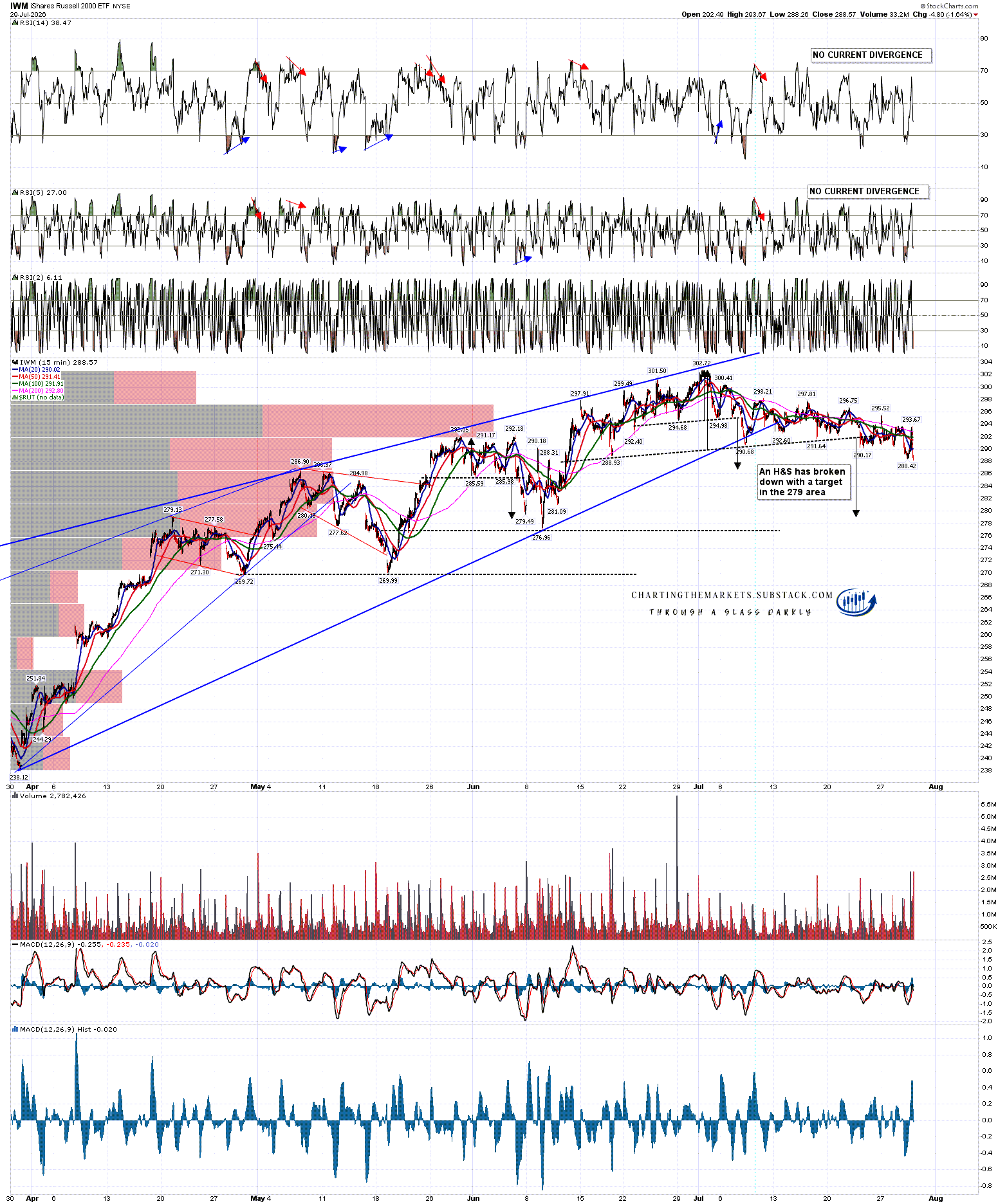

The H&S on IWM failed today and that gives IWM a possible target at a retest of the all time high.

On the bear side there is also a possible alternate H&S right shoulder forming so that ATH retest need not necessarily be seen.

While the three indices above all had their topping patterns fail, the three remaining topping patterns on the charts below still look just fine and are the key to the current inflection point.

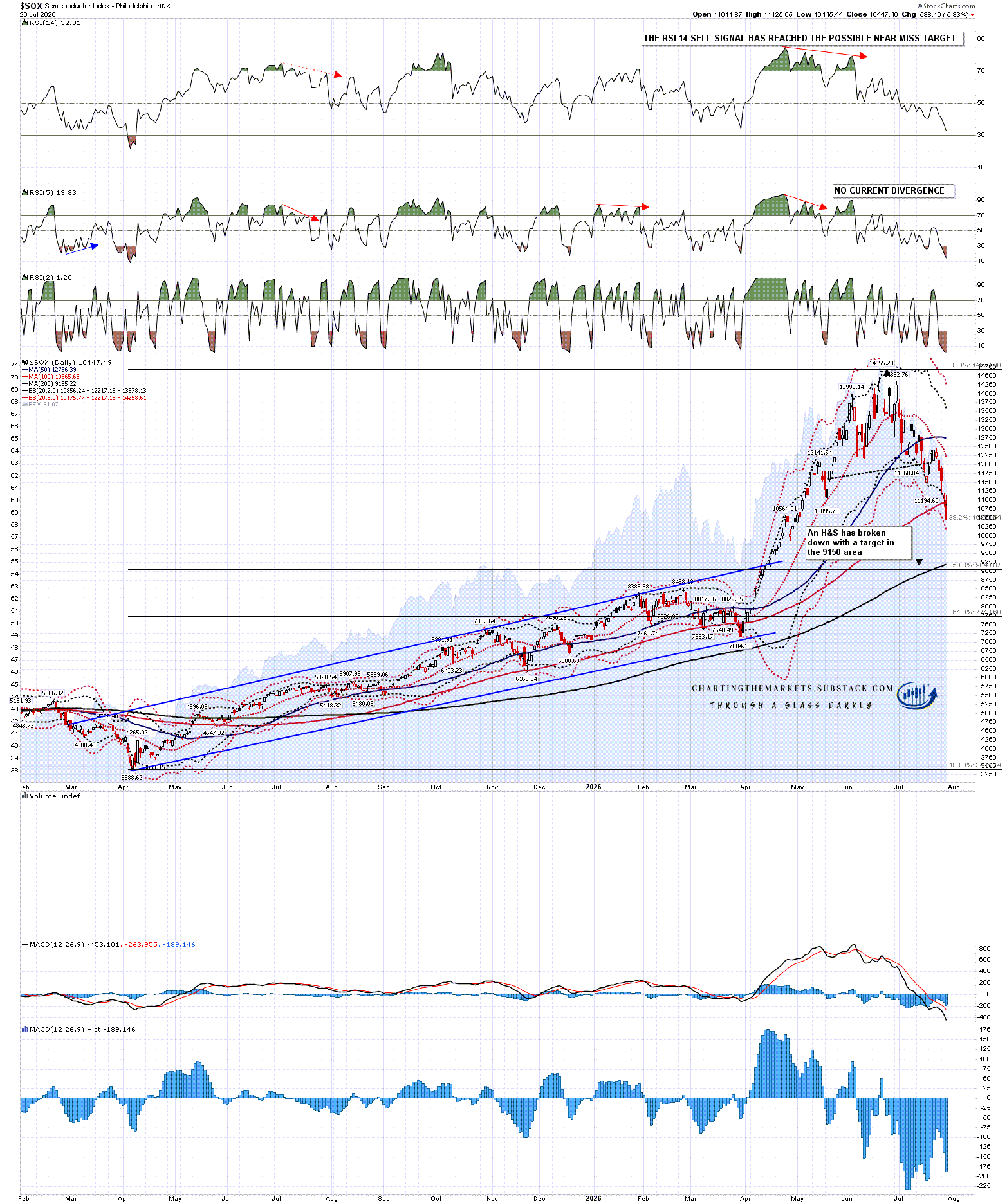

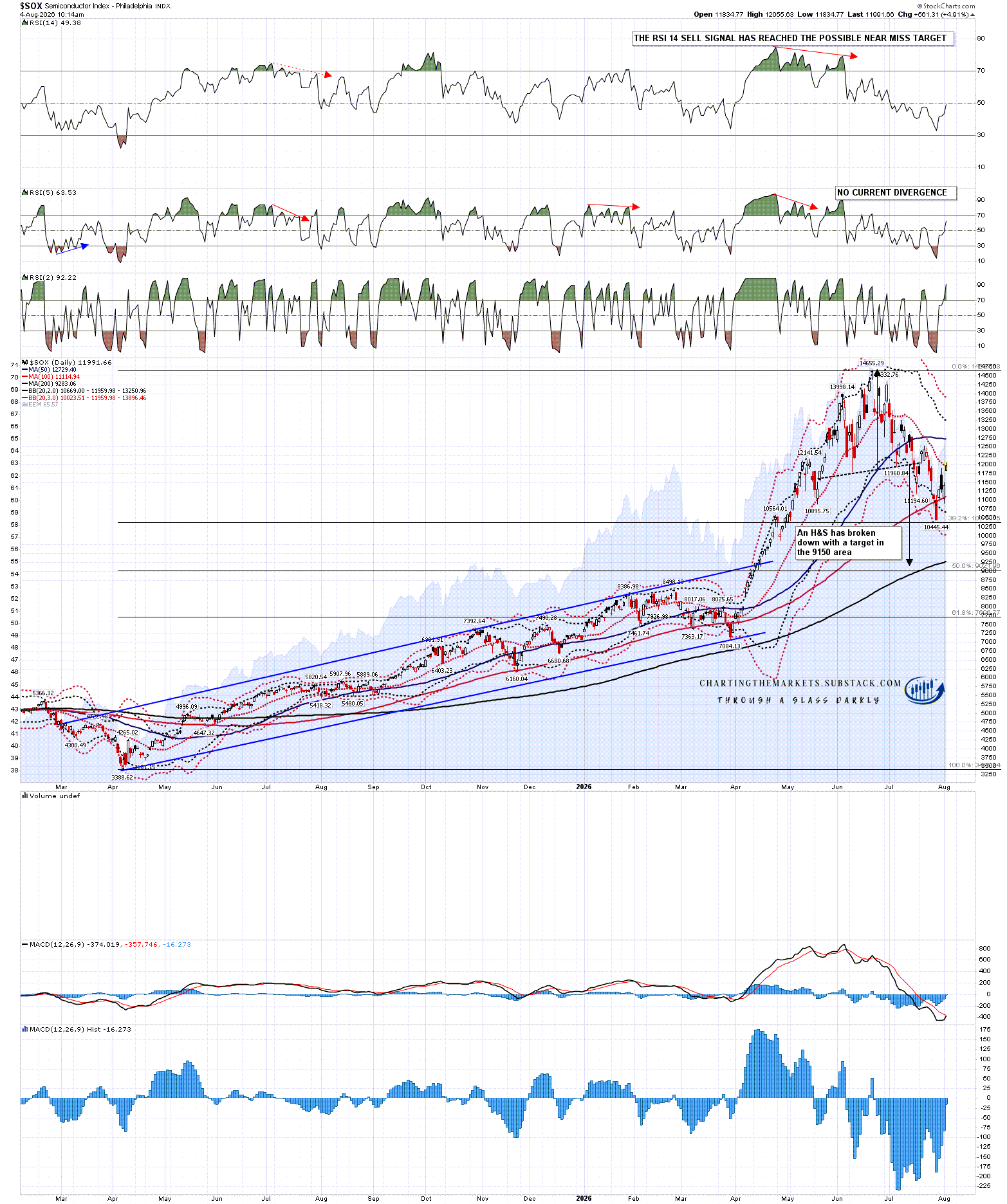

On the Philadelphia Semiconductor Index (SOX) an H&S has broken down with a target in the 9510 area and that currently looks fine. SOX is testing the daily middle band and on a break above I’d be watching for a possible move over the right shoulder high in the 13,249.07 to invalidate the H&S. If we see that, and Tech stops lagging the rest of the market, we might see a genuine break up. That test isn’t close yet though.

SOX daily chart:

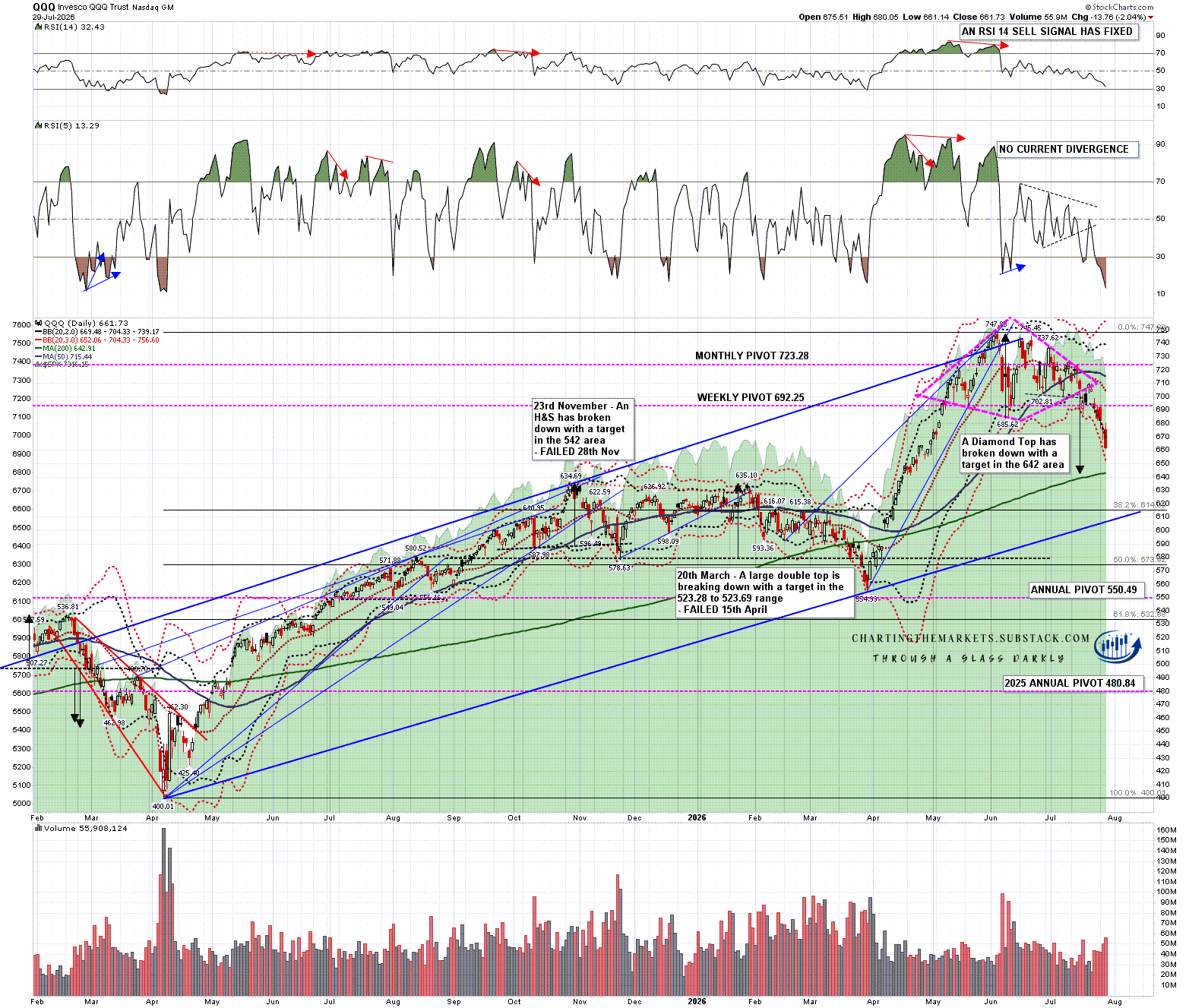

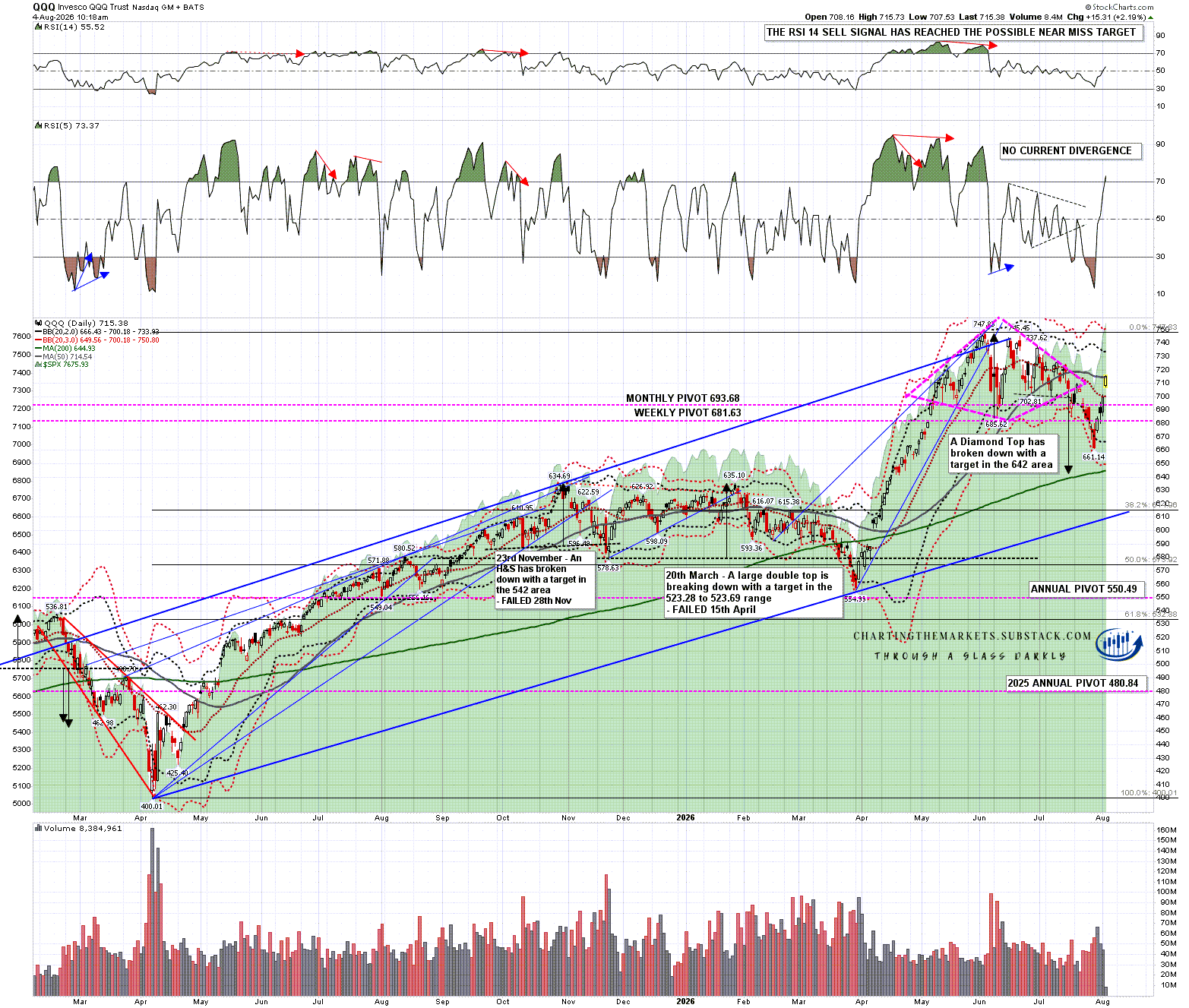

Looking at QQQ we saw a decent break back over the daily middle band this morning into a backtest of the 50dma. A diamond top has broken down with a target in the 642 area and that topping pattern still looks fine. As with SOX, if Tech stops lagging the rest of the market, we might see a genuine break up, so we will see what happens next.

QQQ daily chart:

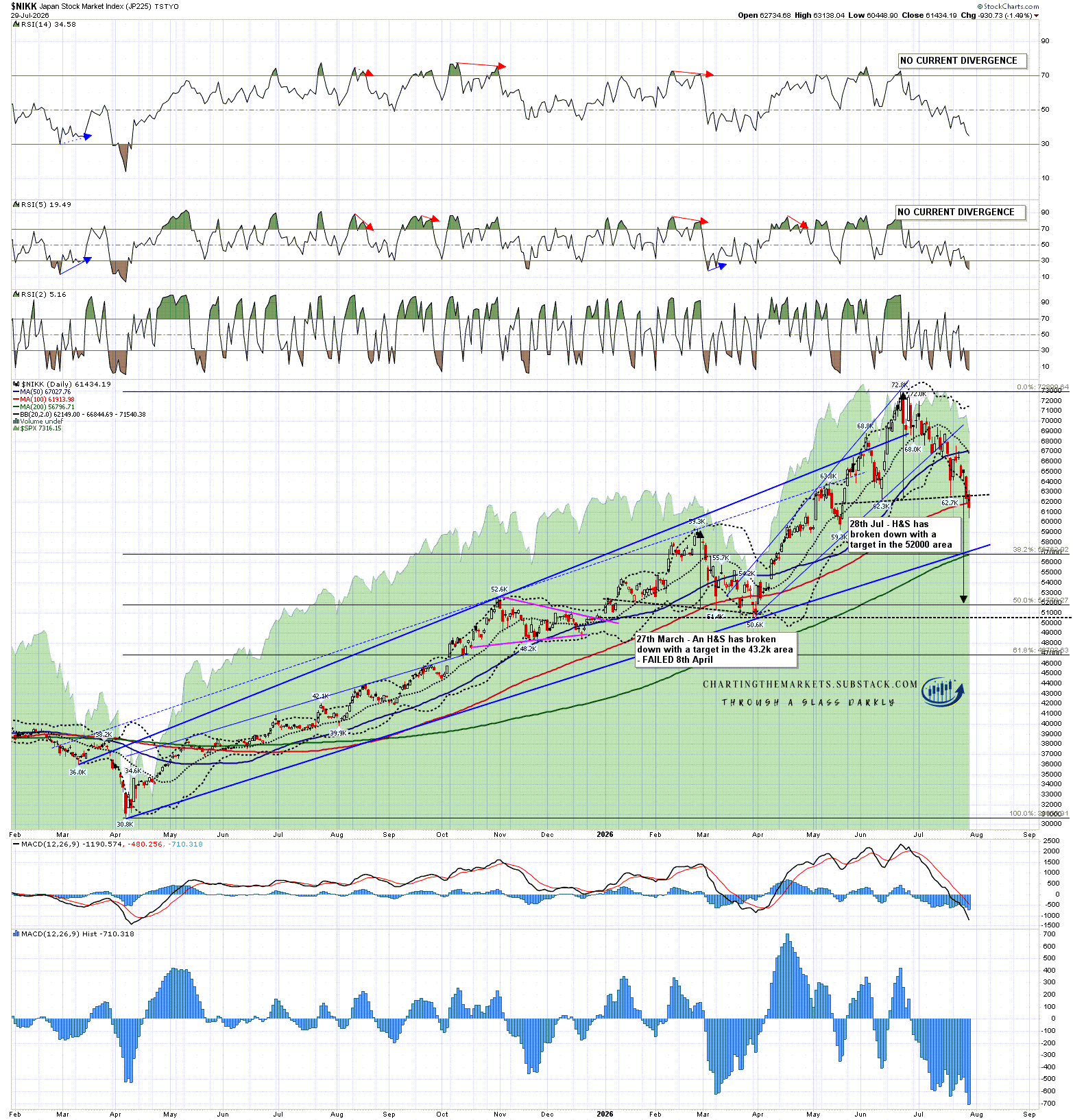

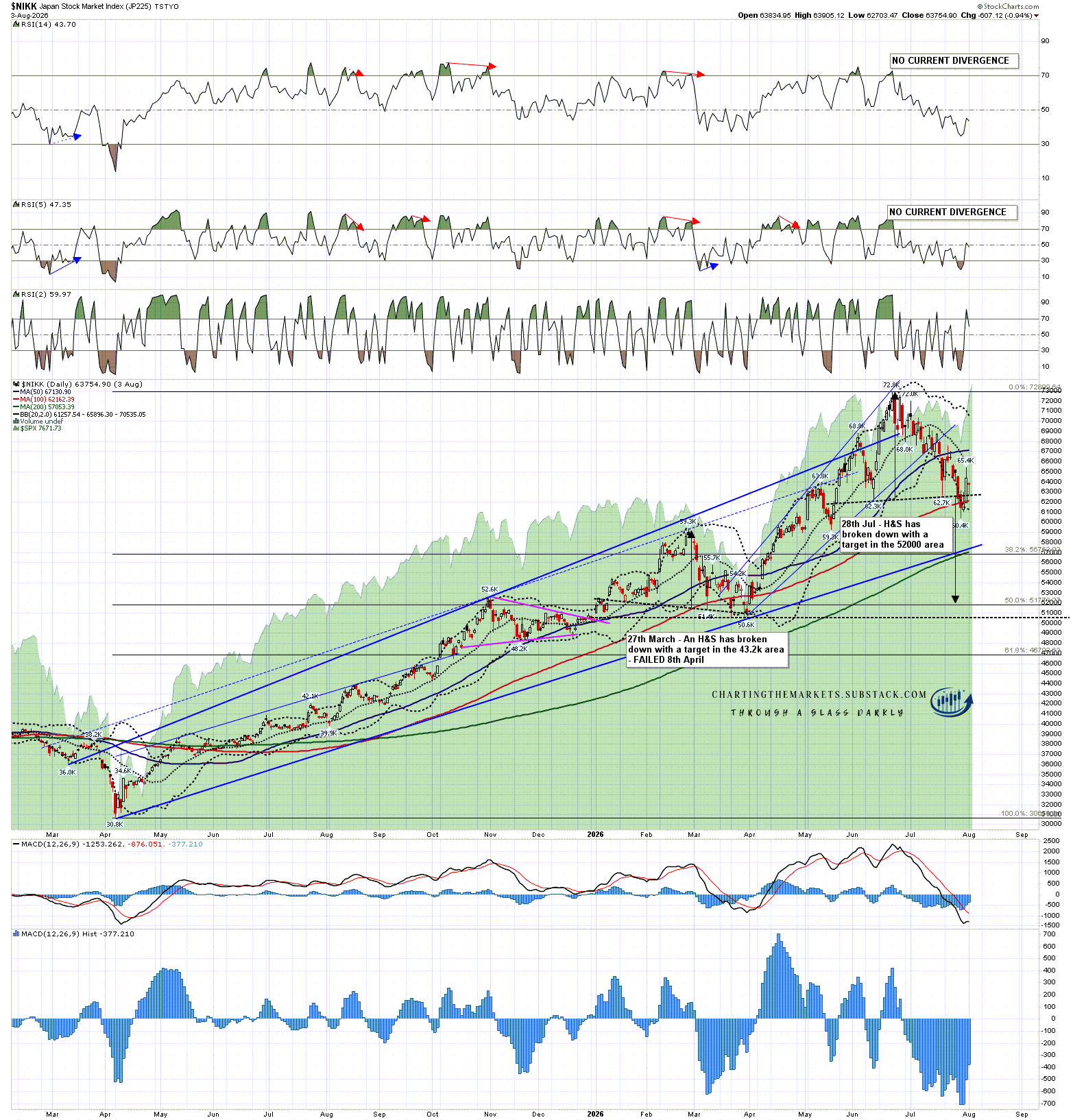

The last chart of the day is the Nikkei 225, looking beyond US markets but it’s worth looking further afield, particularly as DAX and ESTX50 both just retested their all time highs and formed decent quality possible double tops.

On NIKK an H&S broke down last week with a target in the 52000 area. That H&S still looks just fine as well, with NIKK still well below the daily middle band and 50dma. All of these three charts on SOX, QQQ & NIKK still lean bearish and that may well not change.

NIKK daily chart:

So that is the inflection point here. On the bull side we would likely see a consolidation in the current area on SPX and DIA for a week or two, to give room for the daily 3sd upper bands to rise, and then go higher, likely sustained by a Tech sector returning to retest the current all time highs.

On the bear side the downside patterns on SOX, QQQ and NIKK are just seeing a rally here, and the topping patterns on SPX, DIA and IWM have all been improved by the move up since last Wednesday, backed up by new double top setups on DAX and ESTX50 that have now also now formed and might start playing out.

We will see which way this goes and I’m planning another post for tomorrow looking at possible upside targets on SPX, DIA and IWM in the event that US equity markets go higher.

I have very real doubts about that move higher, as the Iran War for now appears to be an insoluble quagmire, the Tech sector is having genuine issues with Chinese innovations and massive capex plans causing serious market concerns, and US bond yields are on a very clear and sustained bullish track that may go a lot further. As always time will tell.

If you like my analysis and would like to see more, please take a free subscription at my chartingthemarkets substack, where I publish these posts first. I also do a premarket video every day on equity indices, bonds, currencies, energies, precious commodities and other commodities at 8.45am EST, but only for paying subscribers. Other places to find me are my page on the platform previously known as twitter, and my YouTube channel.