I’ve been mulling over how to do this post for a while because I don’t want to offend readers who might be very sensitive to any criticism, direct or implied, of the Trump administration, and I tend to stay away from any political discussions. However, any objective review of the likely effect of some of that administration’s policies requires an honest discussion of those policies and their likely impact.

Given that I now believe that the odds of seeing a serious bear market this year are high and that a full market crash is increasingly on the cards. I need to do that objective review, and my apologies if anyone is offended. I am just describing the geopolitical and economic realities here as I see them, and am not planning to make political commentary a regular feature in my analysis going forward.

Lastly, the purpose of this post is to explain my rationale for thinking that a serious bear market this year is likely and that a full market crash is on the cards, to be read before my follow-on post today looking at the likely targets in either of those scenarios. If you are happy to take my word for this and/or don’t enjoy economic analysis then read no further. The TA part of this analysis will be published later today on my main charting substack Charting The Markets and will be entitled April Fools, so move on to look for that there.

THE YEAR SO FAR

After Trump won the election in November I mentioned repeatedly in my posts that this was likely to be a particularly interesting year on the markets because it was the intention of the incoming administration to be revolutionary and disruptive rather than evolutionary and, in that respect at least, this administration has not disappointed. Since the inauguration the geopolitical world political and economic orders have been shaken to their very foundations, and the foundations of a new world order may well be starting to form here.

Is that a bad thing? Not necessarily, the post Cold War settlement has been failing to deliver economically for much of the free world for decades, and the rise of China meant that the days of the US being the sole world superpower were already numbered so, as I mentioned in my posts after the election, the existing world order likely needed a good shake. Out of this (hopefully creative) destruction I’m looking for a rebalancing of the world economy and political order and a better foundation for prosperity in the future. That rebalancing is likely just getting started in my view and may take a decade or two to fully settle down in a new form.

It would be hard to overstate the impact of this revolution so far on the world around us. On the morning after the inauguration Trump woke up as the leader of the free world, the leader of the most powerful military alliance in history (NATO), and as the leader of the greatest trading alliance in history (WTO). Since then Trump has effectively walked the US away from the leadership of the free world and NATO, in effect torn up the free trade agreement with Canada and Mexico, and walked away from the WTO, among other less important world institutions.

This is having a huge impact. In NATO, where the US has effectively now left an empty chair at the head of the NATO table, and Trump has both said repeatedly that the US no longer feels bound by the mutual defence NATO Article 5, and even refused to rule out military action against two NATO allies, Canada and Denmark over territorial demands against Canada and Greenland, former NATO allies have realised that for now at least, the US is no longer a reliable ally and may in fact be evolving into an adversary.

With Trump’s actions regarding Ukraine, the consensus view in Europe is now that Europe has moved from a post-war (WW2) footing to a pre-war footing (perhaps WW3 defending Europe against Russia), and that Europe’s past trust in the US to be their main supplier of weapons may have been a very serious mistake. Europe is starting to now rearm against the current fascist dictator with dreams of empire in Europe, in the expectation that the US may no longer be an ally in that conflict and may even be hostile.

That brings us to the trade disruptions. So far these have been relatively minor, mainly directed against Canada, Mexico, Aluminium and Steel, and that has prompted a correction in US equity indices of 10% so far and some economic disruption. However the tariffs are scheduled to be widened to most of the major trade partners of the US on Wednesday 2nd April, and a 25% tax on imported cars and car parts has already been announced this week to be implemented as part of that.

TARIFFS AS A POLICY TOOL

In terms of assessing tariffs as a policy tool I will defer to Ronald Reagan, in a speech in 1987 as the US was renegotiating trade terms with Japan.

President Reagan's Radio Address on Free and Fair Trade on April 25, 1987

There is also a pretty decent summary given by the Tax Policy Center here, but to sum these up the cost of tariffs is generally paid by buyers of the tariffed goods or services, unless or until they buy from alternative non-tariffed suppliers, if available or competitive with those tariffed prices. Tariffs imposed by the US will restrict and alter trade but is, in essence, a tax on US consumers and businesses.

THE TRADE WAR CLIFF

As Trump has mentioned regularly, tariffs were a very important tool in the nineteenth century in the US and across the world. They were still significant in the twentieth century, with a big move towards protectionism in the decade before WW2 from the US Smoot-Hawley Tariff Act in 1930. That was a total disaster that was a key factor in turning a recession in 1930 into The Great Depression, so there was a free trade consensus in reaction to that after WW2. Since then tariffs had dwindled mostly into insignificance across most of the world until now.

Trump’s intention is for the US to become more isolationist and for some protectionist policies to return in the longer term, particularly in order to return more manufacturing to the US. That’s not inherently a bad thing in my view. The world was in any case heading towards a more multi-polar world, with the US status as the sole world superpower likely to end whatever else happened in the next decade or two, and in that multi-polar world without a single guarantor of peace, countries will need to have much more strategic manufacturing of key goods at home or done by trusted allies to guard against the higher risk of supply chain disruption.

However there is more than one way to move towards that. I was talking to a Trump supporter friend of mine a couple of days ago about tariffs and I said that it wasn’t the aims I have an issue with so much as the proposed method. I compared it to a man standing at the top of a tall cliff who needs to get to the bottom. The easiest and fastest way to get to the bottom is simply to step off the cliff, but that way comes with some clear disadvantages that mean that it is well worth investigating any other potential routes first.

Is some of the trade conducted by the US with trading partners unfair? For sure, but the other path would be to negotiate those imbalances one trading partner at a time with trade war being the alternative option in the event that those negotiations failed. Instead Trump seems to be planning to launch a trade war with the rest of the world first, and then negotiate afterwards.

At the least this is a brave move, as while no individual trade partner is a huge part of the US economy, trade as a whole is 24% of the US economy. There is therefore a large potential for major economic disruption to the US economy as part of a general trade war waged by the US on the rest of the trading world.

When Trump started acting against Canada there were talking heads saying that Canada was in a weak position because while trade with the US was a large part of the economy for Canada, trade with Canada was only a small part of the economy for the US.

Going into a trade war with all trading partners reverses this math. Trade with the US is for instance about 4-5% of the EU’s economy, and that is the largest trading partner of the US. Trade with everyone however is 24% of the US economy.

Trump’s plan seems to be that the US would unilaterally impose tariffs against each trading partner, and in the event that there was any retaliation against those initial tariffs by any trading partners, then the US would retaliate against that retaliation with punitive further tariffs. There seems to be an underlying assumption that most trade partners would not retaliate against those initial US tariffs and that any disruption would therefore be minor.

This seems very optimistic, and the tariffs levied so far against:

The European Union (18% of all US trade 2024)

Canada (14.3% of all US trade 2024 )

China (10.9% of all US trade 2024)

…. have all been retaliated against with tariffs against the US and promises of tit for tat tariffs levied against any further tariffs . That may also be the case with many of the other major US trading partners who are:

Mexico (15.7% of all US trade 2024)

Japan (4.2% of all US trade 2024)

South Korea (3.7% of all US trade 2024)

Taiwan (3% of all US trade 2024)

UK (2.8% of all US trade 2024)

Vietnam (2.8% of all US trade 2024)

India (2.4% of all US trade 2024)

Brazil (1.7% of all US trade 2024)

Singapore (1.7% of all US trade 2024)

Switzerland (1.7% of all US trade 2024)

Thailand (1.5% of all US trade 2024)

Malaysia (1.5% of all US trade 2024)

Between them these fifteen top US trading partners account for 82.2% of all US trade. It may be though that possible exceptions of Mexico (too scared to retaliate much so far), Japan, South Korea & Taiwan (still thinking, possibly correctly, that the US may be still be their vital military ally that they cannot afford to offend), Vietnam, India, Thailand and Malaysia (possibly also economically small enough to bully) and the UK, Brazil and Singapore (all currently buying more from the US than they sell so possibly exempt from further tariffs). Excluding those eleven, the trading partners already or almost certain to retaliate against US tariffs come to at least 44% of US trade volume. Given that there is also a growing global boycott of US goods in response to this trade war I’ll very generously round for working purposes that to 50% or so of US trade that may be significantly or very badly affected by this trade war.

With US trade accounting for 24% of the economy, that gives us a conservative working number at 12% or more of the US economy that may be seriously disrupted, and that brings us to the next section.

THE LIKELY RECESSION COMING IN THE US

In retrospect, there were strong signs that a recession in the US may have been on the way in any case this year before Trump was inaugurated, but the uncertainty since then has now made that much more likely, with consumer confidence falling hard on expectations of a weaker economy and business investment expectations falling due to the uncertainty about US policy, the tax regime, and business conditions going forward. In this situation consumers spend less and businesses invest less, weakening economic activity and making that recession much more likely. At this point the recession may well have already started.

In terms of the consumer confidence numbers I show the latest ones below with a cut-off date for results on 19th March. I would particularly draw your attention to the Expectations index, which has tumbled down about 20 in the last two months to a level strongly indicating recession. If A full trade war really is starting next week then may well drop a lot further into the next numbers.

There’s more though, I calculated above that in the event of a trade war 12% or more of the US economy would be seriously disrupted, but there is more to add to that.

The US government’s Bureau of Economic Analysis is getting harder to get data from due to ‘budget constraints’ but as of Q3 2023 federal spending to GDP there was about 23%, divided between mandatory/entitlement spending, discretionary spending, and interest on government debt. Obviously this is also vulnerable to serious disruption as a lot of federal employees are being downsized and budgets are cut. Total GDP in 2024 would have been in the $28.3tn area, with total federal spending therefore in the $6.5tn area. Elon Musk is hoping to cut $2tn from that and while that seems ambitious it is certain that none of that will be coming from paying interest on the national debt. One way or another a lot of federal jobs and spending are likely to be cut

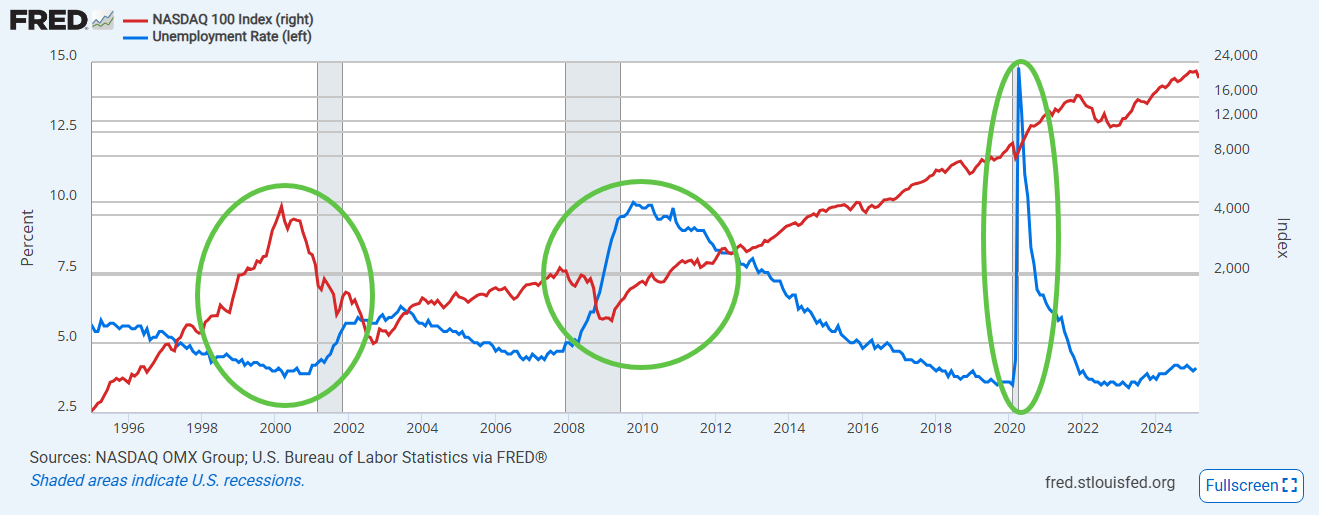

Between trade and federal spending 35% to 47% of the US economy is likely to be seriously disrupted and a lot of jobs lost at a point when the economy is already likely to be entering a recession. This feeds back into markets and the markets feed back into this. You can see this on the FRED (St Louis Fed) chart tracking the Nasdaq 100 and unemployment against the three recessions in the US since 1995. The economy and markets are a delicate system that don’t react well to big shocks.

As this is all being done at the same time this may therefore develop into a major economic shock and a consequently much deeper and more protracted recession.

INFLATION OUTLOOK

What effect does all this have on inflation? There are three main parts to that.

The first part and the ‘good’ news is that recessions and falling demand reduce inflation, with the recent official inflation numbers likely overstated.

The second part is that tariffs increase prices to consumers and businesses, and that is most definitely inflationary, and will reduce consumer spending further. For illustration the estimates of the costs of the tariffs on the ticket prices on new cars that I have seen are high, starting at about $3,000 per car sold and rising a lot from there as foreign made content increases. This will affect almost all cars sold in the US with the smallest effect likely to be on Tesla, though all cars manufactured in the US will also be affected by the tariffs on steel and aluminium. Price rises will be steep, fewer cars will be sold, economic activity will decrease.

The third part is the effect on the US dollar. Now that is an interesting one. Trump wants a lower US dollar to make US exports cheaper and imports more expensive. Obviously that would also be inflationary. There’s more though and that takes us to the last section here:

THE US DOLLAR AND INTEREST RATES

The US dollar has been artificially high for many decades now because the US Dollar is the reserve currency for much of the world. This is a large part of the reason that the US has been running a trade deficit for decades. If the US is withdrawing from world trade to a large degree as seems to be the plan, then there isn’t much point using the US dollar as a reserve currency any more, and alternatives will likely be found. This will depress the US dollar, and that will in turn reduce the trade deficit BUT ….

Other countries hold their dollars in US treasury bills and that keeps bond yields lower than they otherwise would be, and they hold a lot of them, somewhere in the region of $7-8tn of then, so over 25% of the $28tn of US treasury bills outstanding.

What happens when they sell them? Well US treasury prices go down and interest rates in the US go up, as the practical interest rate in the US on which loans & mortgages are based is either the US treasury ten year yield or (long term mortgages) the thirty year yield. Trading partners may also reach a decision to sell faster because either they are retaliating against US tariffs or they want to sell first to avoid selling when the US dollar is lower.

What is the practical effect of this? US dollar goes down, interest rates go up regardless of what the Fed does, as it is really the bond markets that set interest rates. Back in November I was writing about an interesting possible chart setup on TNX suggesting that US interest rates might break up towards 8% & maybe this is the way that happens.

The US dollar going down makes imports even more expensive, on top of tariffs which also drives up inflation.

SUMMARY

There is a very serious possibility that the effects of Trump’s proposed tariffs, if maintained more than a couple of months will be:

Much slowed growth and likely recession

Higher prices to the consumer resulting in inflation

Higher interest rates

What will be the effect on the rest of the trading world? Not huge, US trade is 5% of the Chinese & German economies but falls elsewhere. The only two nations very vulnerable are Canada and Mexico and, over time, both of those can likely move their business elsewhere, particularly Canada, which exports a lot of energy and food. It’s unlikely that these trading partners will start trade wars against each other. Everyone remembers that is how the Great Depression started in the US and was exported worldwide. Likely the rest of the world will just trade more with each other and the US becomes a trading backwater if protectionism becomes long term policy in the US.

What are the likely effects on the US? Hard to say but likely in a range somewhere between bad and disastrous. This is, after all, how the Great Depression really got going in the 1930s. All things pass but it could get very rough and I am wondering if we could see a 5% decline in US GDP over the next year if tariffs and cuts in government spending are implemented strongly and at the same time. What could happen to markets if the US economy catches a severe cold?

If you like my analysis and would like to see more, please take a free subscription at my thebiggerpicture substack, where I publish these posts first and do bi-weekly videos looking at equity indices, bonds, currencies and commodities. If you’d like to see those I post the links on Wednesday and Sunday evenings on my twitter, and the videos are posted on my Youtube channel. The follow up post to this post looking at possible downside targets this year on US equities if we see serious market disruption will be posted at my chartingthemarkets substack.

No comments:

Post a Comment