I’ve written well over two thousand posts over the last sixteen years, and this will be the first that doesn’t include any charts that I drew myself. That feels a bit strange but I’m writing this post to draw everyone’s attention to what is really important about this Iran War.

The war itself is largely irrelevant. Whether the US, Israel or Iran are bombing, or blockading, or blustering doesn’t really matter. All that is really important on the bigger picture are the Strait of Hormuz and, to a slightly lesser extent, the Bab al-Mandab Strait, the two key chokepoints for world trade routes in the Middle East:

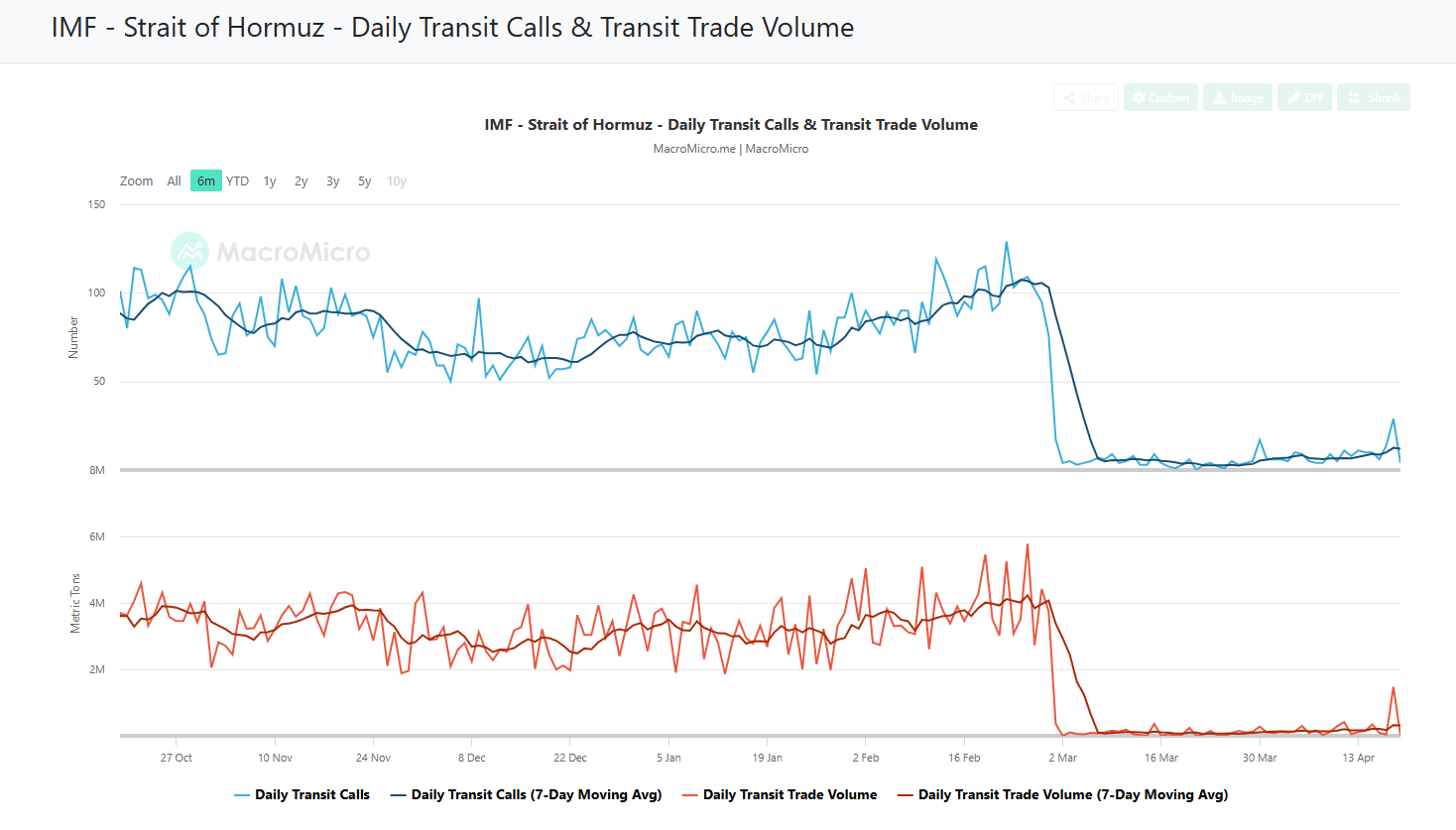

What is important here is that the amount of tankers and trade volume through these Straits, and that traffic through the Strait of Hormuz dropped over 90% at the start of this war and has on average remained at or below that level since then.

To put that in perspective the last oil tanker that passed through the Strait of Hormuz before this war started delivered that cargo on Monday 20th April. After the war started there was a grace period while the tankers still on the sea delivered their cargoes. That grace period has now ended and the Strait is still closed.

There are still oil reserves that have been released to work through, but once they are used up this supply shock will be fully on, and prices will rise to destroy demand until supply and demand for oil balance again. That is what an oil shock is really about.

There are two previous oil supply shocks historically to compare this crisis with, the first in the 1970s and the second when Iraq invaded Kuwait in 1990. In terms of the percentage of world oil supply disrupted both were smaller, and this disruption is already close to lasting longer than in 1990 and may yet last longer than the five months in 1973.

The summary below looks at what happened in these two previous supply shocks to oil prices, equity valuations, GDP and inflation and it is grim reading:

It isn’t just about oil of course, 30% of helium worldwide comes from Qatar and and much of that capacity has been damaged in this war and will be offline for years. That capacity is not obviously even possible to replace, as it is produced as a byproduct of Natural Gas, and prices have already risen over 50% in the demand destruction cycle to balance supply and demand. Helium is vital to semiconductor manufacturing among other uses.

Other major disruptions include aluminium and urea, which is very important for fertilisers. The chart below is Urea prices from the start of 2022, rising rapidly back towards the 2022 highs. This will restrict world food production and deliver higher food prices that will feed though (no pun intended) over the next few months:

In terms of the impact on equity prices, the milder outcome was in 1990 when stocks were slightly overvalued and stocks dropped 21% peak to trough. In 1973 stocks were somewhat more overvalued and markets dropped 52% peak to trough over the next two years, only recovering to the previous highs after seven years.

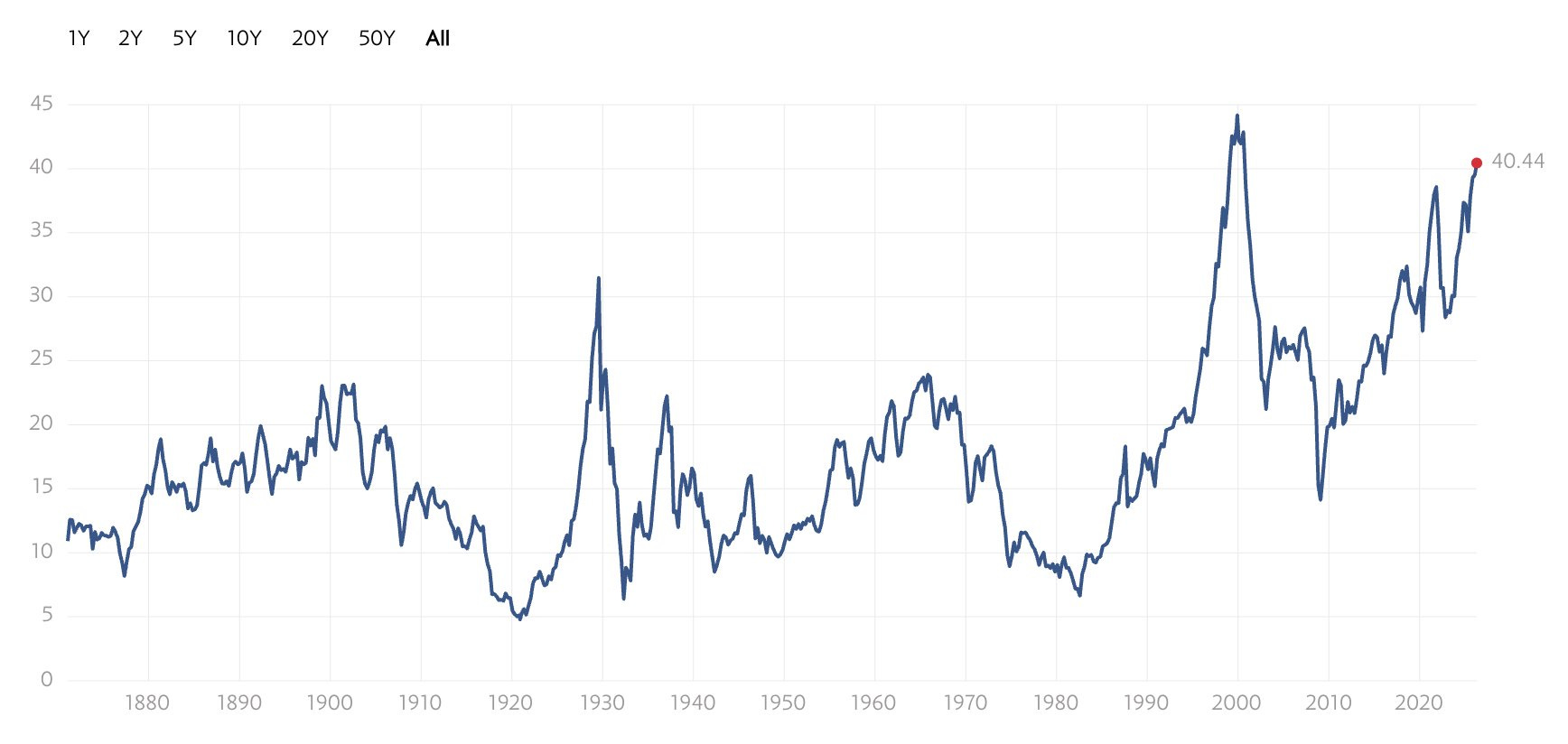

So are stocks overvalued now? Well the chart below is the Schiller P/E ratio since 1870. The current level is 20% higher than the high in 1929, and about 10% lower than the all time high in 2000. For comparison the Schiller P/E ratio was at about 18 in 1973, and 17 in 1990 against a historical mean (before 1990) in the 14% to 15% area. It is currently over 40. There is a strong argument that stocks are extremely overvalued here.

How fragile is the market? Are market expectations diverging from the real economy? The chart below is a look at the S&P and Consumer Sentiment since the start of 2007. It is a thought-provoking chart:

The bottom line here is that all that really matters here is the supply shock to the world from this war in the Middle East. Nothing else is of global importance. Until commerce is flowing freely through these Straits, whether or not Iran is charging a toll, the world is exposed to a severe economic shock , stagnation and inflation. The US is a large oil exporter and is more insulated from this crisis than many, but is a long long long way from immune.

Once this supply shock ends we can see how bad this shock is likely to be as the effects feed through over the next few months and years. So far the speed of international trade has insulated the world from this supply shock but that won’t be the case going forward.

We have yet to see the real effects of this Iran War, and it is important to remember that the news about the war that we see every day is mostly just noise, of no real importance on the bigger picture here.

Overall this situation reminds me of a joke my father used to tell. A man jumps off the top of the Empire State Building and halfway down the building is heard to say ‘so far, so good’. It isn’t the fall that kills you, it’s the landing. That is the thing to focus on.

If you like my analysis and would like to see more, please take a free subscription at my thebiggerpicture substack, where I publish these posts first and for members (from next week) also bi-weekly videos looking at equity indices, bonds, currencies and commodities. Those videos are posted on my Youtube channel after a seven day delay. Links to all my posts from my charting substacks are also always posted on my twitter.

No comments:

Post a Comment